What if your dream of a sun-drenched outdoor sanctuary became a legal nightmare because of a single missing document? For many homeowners, the leap from an aspirational design to a finished patio feels fraught with risk, especially when QBCC home warranty insurance addresses thousands of claims annually to resolve residential construction defects. You want to elevate your lifestyle without the lingering anxiety of structural flaws appearing years after the final coat of oil has dried. It’s natural to feel protective of your investment when the stakes for your home’s well-being are this high.

This 2026 qbcc home warranty insurance guide provides the clarity you need to move forward with absolute confidence. You’ll learn how to navigate the mandatory premium structures and the vital six year and six month protection window that secures your outdoor space against major defects. We will walk you through the essential steps to verify your contractor’s credentials and the precise process for making a claim; ensuring your journey toward a seamless indoor-outdoor transition remains as refined and stress-free as the destination itself.

Key Takeaways

- Secure your vision of a perfect outdoor sanctuary by understanding how the mandatory Queensland Home Warranty Scheme safeguards your high-end patio investment against unforeseen structural issues.

- Utilise our comprehensive qbcc home warranty insurance guide to distinguish between protected structural builds and cosmetic softscaping, ensuring every element of your project meets Australian standards.

- Learn how to verify that your contractor has fulfilled their legal obligation to pay the insurance premium, a critical step in preserving the long-term value and integrity of your home.

- Navigate the resolution process with confidence by discovering how the QBCC acts as a professional mediator to rectify defects and maintain the seamless flow of your lifestyle space.

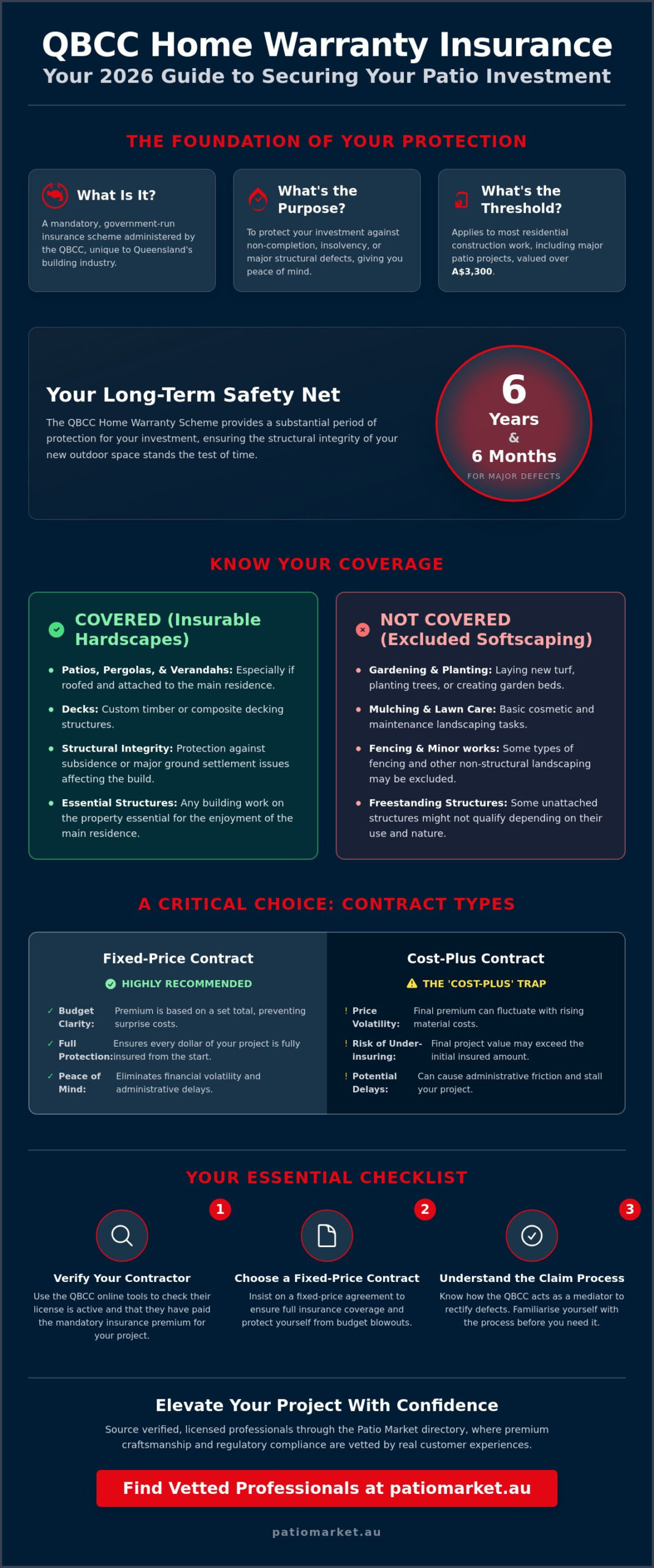

- Elevate your project by sourcing verified, licensed professionals through the Patio Market directory, where premium craftsmanship and regulatory compliance are vetted by real customer experiences.

Understanding the Queensland Home Warranty Scheme in 2026

Creating an outdoor sanctuary requires more than just premium materials; it demands the peace of mind that comes with legal security. In 2026, the Queensland Building and Construction Commission (QBCC) continues to administer a mandatory statutory insurance scheme that stands as a unique pillar of the local building industry. This qbcc home warranty insurance guide outlines how this protection transforms a vulnerable construction zone into a secure investment. Unlike other states, Queensland’s scheme is managed directly by the government, providing a robust safety net for residential projects valued over A$3,300. This threshold ensures that even modest lifestyle upgrades receive the same level of oversight as major renovations. It turns the stressful building site phase into a journey toward a refined living space where quality is guaranteed by law.

The Purpose of the Statutory Insurance Scheme

Designing a bespoke outdoor retreat involves significant emotional and financial investment. The QBCC scheme protects this commitment by covering the non-completion of work if a builder becomes insolvent or loses their license. It safeguards the structural integrity of your project against defects that could compromise your safety or the aesthetic flow of your home. For those embarking on home improvement projects, this coverage extends to critical issues like subsidence or settlement. These unforeseen ground movements can ruin expensive tiling or masonry, yet the insurance ensures your sanctuary remains stable for years to come. It acts as a promise that your investment in craftsmanship is shielded from the unpredictability of the construction industry, allowing you to focus on the joy of your new space.

Fixed-Price vs. Cost-Plus Contracts

Selecting the right contract structure is as vital as choosing the right weather-resistant timber for your deck. Fixed-price contracts provide a definitive premium based on a set total, offering clarity for your budget and insurance coverage depth. Conversely, cost-plus contracts often introduce volatility into high-end patio builds because the final insurance premium may fluctuate as material costs rise. While the flexibility of cost-plus arrangements appeals to some, they often lack the price certainty required for precise premium calculations. This can lead to administrative delays that stall your project’s progress. The “Cost-Plus” trap for homeowners in 2026 is the risk of under-insuring a project because the final value exceeds the initial estimate provided to the QBCC. This qbcc home warranty insurance guide recommends sticking to fixed-price agreements to ensure every dollar of your craftsmanship is fully protected. A fixed-price approach ensures the transition from indoor to outdoor living is as seamless and secure as possible.

What is Covered? The A-Z of Insurable Outdoor Work

Creating a sanctuary requires more than just vision; it demands structural integrity and a commitment to quality. Under the Queensland Building and Construction Commission Act 1991, the insurance scheme covers residential construction work exceeding A$3,300 in value. This protection applies to structures attached to your home or those essential to its enjoyment on the same land. While “softscaping” like planting, mulching, or basic lawn care doesn’t qualify for coverage, the hardscapes that form the bones of your outdoor room are firmly protected. Understanding these boundaries is an essential part of any qbcc home warranty insurance guide for the modern homeowner.

The “Main Residence” rule is a pivotal factor in determining your coverage. Work performed “on the site” of a residence generally falls under the scheme, provided it involves a building or structure. This means your dream renovation isn’t limited to the four walls of your lounge room. If the project enhances the liveability of your primary dwelling, it likely sits within the protective embrace of the QBCC. You’ll find that structural integrity and aesthetic appeal go hand in hand when your builder adheres to these regulated standards.

Patios, Pergolas, and Verandahs

Elevate your lifestyle with a custom timber deck or a sleek steel patio. These aren’t just additions; they’re seamless extensions of your living space. If your new verandah is roofed and attached to the main house, it’s almost certainly covered by the insurance. Freestanding structures also fall under the requirements of this qbcc home warranty insurance guide if they require a building permit or exceed the A$3,300 threshold. Protecting the craftsmanship of these builds ensures your investment remains a source of joy for years. This coverage specifically guards against structural defects, such as issues with footings or load-bearing beams, for a period of six years and six months from completion.

Outdoor Blinds and Shade Systems

Enhancing your privacy and comfort often involves sophisticated shade solutions. Motorized outdoor blinds and fixed screens are considered “insurable work” when they form part of a larger, managed project like a new patio or a major renovation. High-quality, weather-resistant installations are vital in the Australian climate, where UV exposure and sudden storms test every material. Integrating these elements into your build ensures they’re backed by the same structural warranties as the roof over your head. When you’re ready to curate your outdoor sanctuary with premium finishes, knowing they’re part of a protected project provides genuine peace of mind.

- Structural Coverage: Includes foundations, roofing, and load-bearing timber or steel.

- Cosmetic Exclusions: Does not include garden beds, plants, or decorative pebbles.

- Value Threshold: Coverage kicks in for any building work valued over A$3,300, including GST.

- Duration: Protection lasts for 6 years and 6 months for major defects.

The transition between your indoor and outdoor worlds should be effortless and secure. By focusing on projects that fall within these guidelines, you ensure that your home remains a destination for well-being, backed by the strongest consumer protections in the state. Always verify that your contractor has paid the insurance premium before work begins to keep your sanctuary safe.

Calculating the Investment: Premiums and Responsibilities

Creating a sanctuary requires more than just premium materials; it demands the security of professional oversight. Understanding the financial structure of your protection is a vital part of this qbcc home warranty insurance guide. While the insurance serves as your safety net, the responsibility for activating it lies with your builder. This premium is not an optional extra. It is a mandatory investment in the longevity of your home, calculated as a sliding scale based on the total contract value of your project. For any residential construction work in Queensland valued over A$3,300, this insurance becomes a legal necessity that secures your peace of mind.

Who Pays the QBCC Insurance Premium?

Your builder acts as the essential intermediary for this protection. They must collect the premium from you as part of your initial deposit and remit it to the QBCC within 10 business days of signing the contract. You are the one funding the policy, but the builder holds the administrative duty to ensure the payment reaches the commission. Verification is your most powerful tool. You should always visit the QBCC online register to confirm a valid insurance certificate exists for your specific address. If your contractor fails to provide proof of payment or a certificate of insurance, you must pause the project. Contact the QBCC immediately to rectify the lapse before any physical work begins on your property.

By 2026, the regulatory landscape will shift to offer even greater transparency for homeowners. Builders will be required to provide a formal Notice of Cover before they are permitted to start work on-site. This change reinforces your “Duty of Care” as a property owner. You must act as an informed curator of your home project, ensuring that every legal safeguard is active. Never allow a shovel to touch the earth until you have sighted the digital confirmation in the QBCC portal. This proactive approach ensures the transition from design to construction remains seamless and secure.

Coverage Durations and Limitations

Longevity is a hallmark of superior craftsmanship and timeless design. Under the standards enforced through 2026, structural defects remain covered for a period of 6 years and 6 months. This window begins from the date the premium is paid, the contract is signed, or the work is commenced, whichever happens first. This extensive timeframe ensures your home’s skeletal integrity remains a sanctuary for years to come. It covers major failures that might compromise the safety or stability of the building.

Non-structural issues carry a more focused window of protection. These typically include cosmetic flaws or minor functional defects that do not impact the building’s structural soundness. For these items, the coverage window is significantly shorter, generally spanning 6 months to 1 year from the date of completion. Because the coverage begins the moment the payment is processed, the insurance creates a safety net that spans from the first day of the contract to the final sunset on your new patio. Understanding these specific timelines allows you to manage your investment with the confidence of a seasoned homeowner.

When Things Go Wrong: The Claims and Resolution Process

Creating a home is an act of curation. It’s a way to elevate your daily life into something extraordinary. When the craftsmanship doesn’t meet the high standards you’ve envisioned, the qbcc home warranty insurance guide serves as your essential roadmap to restoration. The process begins the moment you identify a defect. You must notify your builder in writing immediately, allowing them a reasonable opportunity to rectify the issue before the commission steps in as a mediator. This early communication is vital for maintaining the professional relationship while protecting your legal standing.

Documentation is the foundation of a successful resolution. You should capture high-resolution photography that highlights the failure of materials or structural integrity from multiple angles. Professional inspections from independent experts provide the technical weight needed to support your claim, creating a clear timeline of events. If your project fails to commence entirely, the “Loss of Deposit” claim provides a necessary safety net. This allows you to recover up to A$20,000 or 20% of the contract value, ensuring your financial sanctuary remains intact even if the initial builder falters before the first stone is laid.

Filing a Complaint for Defective Work

The QBCC acts with authority through the “Notice to Rectify,” which is a formal instruction that demands a builder correct substandard work within a set timeframe. If a builder disappears through insolvency or loses their license, the path shifts to a direct insurance claim. This provides the necessary funds to complete your home to a professional standard. Owners must also be aware that the deadline for reporting structural subsidence for specific older building schemes is 30 June 2026. Acting before this date is crucial for those managing long-term structural concerns in established properties.

The Adjudication Path

Disputes regarding payments or incomplete milestones don’t have to disrupt your peace of mind forever. The QBCC adjudication process offers a structured, rapid method to resolve contractual disagreements without the heavy burden of traditional litigation. It’s a pragmatic way to ensure everyone is treated fairly. Many homeowners avoid these complications entirely by sourcing contractors through vetted professional directory listings, where high-end craftsmanship and reliability are prerequisites. A seamless resolution ensures that your transition from construction to relaxation is as smooth as possible. To ensure your home is finished with the quality and elegance it deserves, explore premium outdoor solutions from Patio Market today.

Finding Verified Professionals via Patio Market

Creating a sanctuary requires more than just a vision; it demands a foundation of trust and legal certainty. This qbcc home warranty insurance guide has highlighted the technical necessities, but finding a builder who respects these regulations is your next vital step. Patio Market acts as your lifestyle architect, curating a directory where high-end design meets strict Australian compliance. We bridge the gap between your aspirational outdoor goals and the practical requirements of Queensland building laws.

Vetting Your Patio Builder

Our search tools allow you to filter for specific expertise with surgical precision. Whether you’re searching for Stratco patio installers or the best outdoor blinds companies, our platform simplifies the discovery process. Every business profile on Patio Market provides a space to verify the builder’s QBCC license number directly. This transparency ensures you aren’t chasing paperwork during the final stages of your project. Verified vendors are the cornerstone of a stress-free renovation. They understand that any residential project exceeding A$3,300 requires the safety net of home warranty insurance. By choosing a professional who is already vetted, you mitigate the risks that lead to the thousands of construction disputes reported in Queensland each year.

Elevating Your Outdoor Living Experience

A well-executed project moves beyond mere compliance to focus on design, sanctuary, and long-term well-being. When you choose a professional who prioritizes craftsmanship and uses UV-stabilized, weather-resistant materials, you’re investing in your home’s future. A correctly insured project, documented thoroughly through the QBCC, can increase the resale value of a property significantly. It offers future buyers total peace of mind that the structure is sound and protected. We believe in the seamless transition between your indoor comfort and the radiant beauty of the Australian sun. By using this qbcc home warranty insurance guide alongside our directory, you ensure your new patio is a permanent heirloom rather than a temporary addition.

Use this final checklist to hire your next installer with total confidence:

- Confirm the builder’s QBCC license is active and specific to your project type.

- Read customer reviews to assess their history with insurance lodgments and communication.

- Verify the contract price includes the mandatory QBCC insurance premium.

- Ensure the builder provides the insurance notification before any physical work starts on-site.

- Check for a portfolio that demonstrates experience with the harsh Australian climate.

Your outdoor space should be a destination for relaxation, not a source of administrative stress. By partnering with professionals who value both aesthetics and authority, you protect your investment and your lifestyle. Ready to transform your backyard into a luxury retreat? Explore our directory of verified outdoor professionals and start your journey with a partner you can trust.

Secure Your Vision of the Perfect Australian Retreat

Crafting a bespoke outdoor retreat requires a blend of aesthetic vision and rigorous technical standards. This qbcc home warranty insurance guide highlights the vital role of the Queensland Home Warranty Scheme in protecting residential construction projects exceeding A$3,300. By mastering the nuances of coverage, such as the six year and six month protection period for structural defects, you transform a simple renovation into a lasting investment in your well-being. Quality craftsmanship deserves the protection of a verified professional who understands the specific 2026 regulatory environment.

Patio Market simplifies this journey by offering a comprehensive directory of Australian outdoor lifestyle experts. Our curated listings feature verified QBCC license holders who specialize in premium shade and patio solutions designed for the unique Australian climate. We focus on the seamless transition between indoor and outdoor living, ensuring every structural element meets the highest standards of durability and elegance. It’s the most reliable way to connect with builders who prioritize both beauty and compliance.

Find a Verified and Insured Patio Builder on Patio Market to start your project with absolute certainty. It’s time to build the sanctuary you’ve always imagined.

Frequently Asked Questions

Is QBCC home warranty insurance mandatory for all patio builds in 2026?

Yes, QBCC insurance is mandatory for any residential patio construction in 2026 where the total contract value exceeds A$3,300, including GST. This legal requirement ensures your investment in a new outdoor sanctuary remains protected from the moment the first beam is placed. Your builder must collect this premium and pay it to the QBCC on your behalf before work commences on your property.

How much does the QBCC insurance premium cost for a standard A$20,000 patio?

For a standard A$20,000 patio build, the QBCC insurance premium typically falls between A$190 and A$250. These rates are set by the Queensland government and vary based on the total contract value and the builder’s specific license category. You can find the exact figure in the QBCC premium table updated on 1 July 2024, ensuring your budget for a seamless outdoor transition remains precise and transparent.

What happens if my builder goes out of business before finishing my outdoor blinds?

If your contractor ceases trading or enters liquidation before finishing your outdoor blinds, the QBCC insurance scheme provides a safety net for non-completion. You can lodge a claim to have the remaining work finished by another licensed professional. This protection is a core component of our qbcc home warranty insurance guide, offering peace of mind that your vision of a perfect sanctuary won’t be left half-finished due to financial instability.

Can I pay the QBCC insurance premium myself instead of the builder?

You cannot pay the QBCC insurance premium yourself; the licensed contractor responsible for the work must handle this transaction. The law requires the builder to collect the premium from you as part of the initial deposit and remit it to the QBCC within 10 business days of signing the contract. This process ensures the policy is correctly linked to the professional’s license and the specific craftsmanship of your project.

Does the home warranty insurance cover damage caused by storms or fire?

QBCC home warranty insurance doesn’t cover damage resulting from storms, fires, or floods. Its primary purpose is to protect against structural defects and non-completion caused by builder error or insolvency. For protection against the unpredictable Australian elements, you’ll need a comprehensive home and contents insurance policy. Ensure it specifically lists your outdoor structures and high-end furniture as covered assets to maintain your home’s security.

How do I check if my builder has actually paid the insurance premium?

You can verify the payment status by using the QBCC’s online insurance search portal with your property’s address or the builder’s license number. Once the premium is processed, the QBCC issues a Certificate of Insurance directly to you via post or email. It’s a vital step in this qbcc home warranty insurance guide to confirm this document is in your hands before any physical construction begins on your property.

What is the difference between QBCC insurance and standard home and contents insurance?

QBCC insurance covers risks associated with the builder’s performance, such as structural failures or a contractor going bust. Standard home and contents insurance protects your sanctuary from external events like theft, accidental damage, or weather-related destruction. While the QBCC policy safeguards the integrity of the build for 6 years and 6 months, your general insurance provides ongoing security for your daily lifestyle and belongings.

Does the warranty cover fading or wear and tear on outdoor furniture and fabrics?

The warranty doesn’t cover aesthetic wear and tear, fading, or the natural aging of outdoor furniture and fabrics. These elements are subject to the manufacturer’s warranty rather than building insurance. To maintain the elegant look of your sanctuary, we recommend selecting UV-stabilized materials and weather-resistant finishes. These are designed to withstand 300 days of annual Queensland sunshine without losing their sophisticated charm or structural integrity.