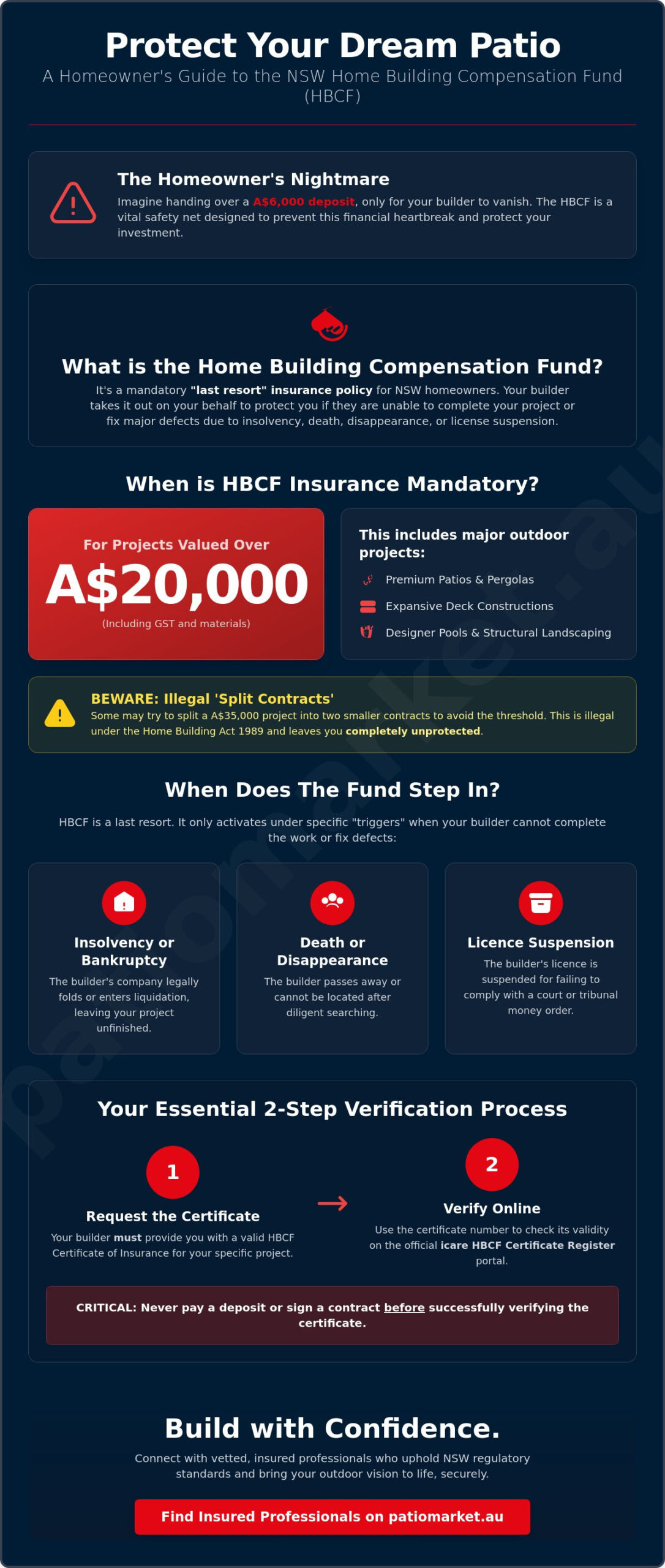

Imagine the quiet heartbreak of handing over a A$6,000 deposit for your dream spotted gum deck, only to discover your builder has vanished into insolvency before the first post is even set. You’ve spent months envisioning this sanctuary as a place to host summer twilight dinners; the thought of your hard-earned savings disappearing is understandably paralyzing. It’s a common anxiety for homeowners, but your journey toward a seamless outdoor lifestyle shouldn’t be defined by fear. Having the home building compensation fund nsw explained is the essential first step in anchoring your project in security rather than uncertainty.

We at Patio Market have curated this guide to transform complex insurance requirements into a clear roadmap for your peace of mind. You’ll learn exactly why any project valued over A$20,000 requires this specific protection and how to verify a certificate of insurance before you sign a single document. We’ll demystify the difference between standard warranties and specialized home building compensation fund coverage. This ensures your investment in premium craftsmanship is legally compliant and protected from the first shovel in the ground to the final sunset on your new patio.

Key Takeaways

- Understand why the HBCF is a vital safety net for your outdoor sanctuary, acting as a final line of defense if your builder is unable to fulfill their obligations.

- Discover if your project requires mandatory insurance by learning how the A$20,000 threshold applies to premium patio builds and designer pool installations.

- Get the home building compensation fund nsw explained to clearly distinguish between standard public liability insurance and the specific protection required for residential labor.

- Master the essential two-step verification process to validate your builder’s insurance certificate through the official icare portal before paying any deposits.

- Learn how to connect with vetted professionals who uphold NSW regulatory standards, ensuring your journey toward a seamless outdoor lifestyle is secure and stress-free.

The Essential Safety Net: What is the Home Building Compensation Fund?

Imagine your home as more than just a structure; it is a carefully curated sanctuary where the boundary between your interior comfort and the vibrancy of the Australian sun dissolves. When you embark on a significant renovation or build a new outdoor retreat, the financial stakes are as high as your aesthetic expectations. This is where the What is home warranty insurance? question becomes vital for every property owner in New South Wales. The Home Building Compensation Fund (HBCF) serves as a mandatory safety net established under the NSW Home Building Act 1989. It applies to most residential building projects valued at over A$20,000, including structural landscaping, swimming pools, and expansive deck constructions.

Having the home building compensation fund nsw explained helps you realize it functions as a “last resort” insurance. This means the policy only triggers when your builder is legally or physically unable to fulfill their contractual obligations. It is not a standard policy you buy yourself; instead, your builder must take it out on your behalf before any work begins or any deposit is paid. Understanding the governance of this scheme ensures you know who to turn to. While icare (Insurance and Care NSW) acts as the service provider issuing the insurance policies, the State Insurance Regulatory Authority (SIRA) serves as the independent regulator. This distinction ensures the system remains transparent and stable for everyone involved in the building process.

Why HBCF is Non-Negotiable for Quality Craftsmanship

Selecting a builder who prioritizes HBCF compliance is the first step in ensuring the longevity of your investment. It separates the dedicated craftsmen from the unlicensed operators. When a builder provides a certificate of insurance, they offer you the emotional peace of mind that your vision for a seamless outdoor lifestyle is backed by a state-managed fund. This protection ensures that the high-end materials and sophisticated designs you choose today remain protected against the unexpected. It is about more than just money; it is about protecting the future sanctuary you are building for your family.

The Four Triggers: When Does the Fund Step In?

The HBCF does not cover simple contractual disputes or minor disagreements over finish. It activates under four specific “triggers” where the builder cannot complete the work or rectify major defects:

- Insolvency or bankruptcy: This occurs when the building company legally folds or enters liquidation, leaving projects in a state of limbo.

- Death or disappearance: The fund provides a practical pathway forward if the builder passes away or cannot be located after diligent searching.

- Licence suspension: Under updated regulations and moving into the 2026 context, the fund can be triggered if a builder’s licence is suspended for failing to comply with a court or tribunal money order in favor of the homeowner.

These specific protections ensure that your path to a refined home environment remains secure, providing a financial bridge to complete your project even if your original builder vanishes from the industry.

Mandatory Thresholds: Does Your Patio Project Require HBCF?

Creating a sanctuary in your backyard often involves significant investment to ensure the transition between your indoor and outdoor living is seamless. In New South Wales, any residential building work valued at over A$20,000, including GST and materials, must be covered by insurance. This home building compensation fund nsw explained simply means that for premium patio installations or designer pools, your builder must provide you with a certificate of insurance before taking any deposit or starting work. This protection is not optional; it is a legal safeguard designed to protect your vision of a perfect home.

Some homeowners feel tempted to bypass this requirement by using ‘split contracts’ to keep individual project values below the A$20,000 mark. Breaking a single A$35,000 deck and pergola project into two separate A$17,500 agreements is illegal under the Home Building Act 1989. This practice leaves you entirely unprotected if the builder disappears or fails to complete the work. For a project to truly elevate your lifestyle, it must be grounded in legal security. Understanding what is icare HBCF helps you realize that the fund acts as a safety net of last resort, offering coverage up to a A$340,000 cap per dwelling for the 2026 period if your builder becomes insolvent, dies, or vanishes.

Defining ‘Residential Building Work’ in an Outdoor Context

The definition of residential work extends far beyond the four walls of your lounge room. In the context of an Australian outdoor lifestyle, it specifically includes the construction of patios, decks, pergolas, and even high-end fencing. If you are simply replacing a few weather-worn boards or performing minor aesthetic repairs under the A$20,000 threshold, insurance isn’t required. However, most structural enhancements that create a lasting outdoor sanctuary will meet the mandatory insurance criteria. Always ensure your contract price includes the full cost of all materials and labor to remain compliant with NSW regulations.

Statutory Warranty Periods: 2 Years vs. 6 Years

Your peace of mind is protected by two distinct warranty windows that cover the craftsmanship of your project. For non-major defects, such as minor cracks in timber or aesthetic finish issues, you are covered for 2 years from the date of completion. For more serious concerns that threaten the integrity of the space, the coverage extends significantly. A major defect is a fault in a structural element that results in the building, or part of it, being unable to be used for its intended purpose or poses a threat of collapse. These structural issues carry a 6-year warranty, ensuring your investment remains a safe and durable destination for well-being for years to come.

HBCF vs. Standard Warranties: A Critical Distinction

Your journey toward a refined outdoor sanctuary involves more than selecting weather-resistant timber or UV-stabilized fabrics. It requires a clear understanding of the legal safeguards that protect your investment. A common misconception is that a builder’s public liability insurance offers the same protection as the Home Building Compensation Fund (HBCF). Public liability covers accidental damage or injury during construction; however, the home building compensation fund nsw explained simply, is a safety net for when the craftsmanship itself is compromised and the builder is no longer able to rectify it.

- Labor vs. Materials: A product warranty covers the physical components, like a high-end awning mechanism, while HBCF protects the structural integrity of the installation labor.

- Mandatory Protection: The Home Building Act 1989 dictates that builders cannot opt-out of this insurance for residential projects exceeding A$20,000, even if a homeowner offers a written waiver.

- Curated Compliance: A professional builder acts as a knowledgeable curator, managing these technical details to ensure your transition from design to reality is effortless and secure.

The Myth of the ‘Self-Insured’ Builder

Some contractors might suggest their personal ‘guarantee’ is sufficient, but this claim lacks legal standing in New South Wales. Commencing work without a valid HBCF certificate is a breach of the law that carries significant penalties, including fines up to A$22,000 for individuals or A$110,000 for corporations. This strict regulation ensures the seamless transition between indoor and outdoor living remains free from legal friction. You shouldn’t accept a verbal promise when the law demands a certificate. It’s the only way to secure the longevity of your sanctuary against unforeseen business failure.

HBCF as a ‘Last Resort’ vs. Active Dispute Resolution

Understanding the rhythmic flow of the claims process is vital for your peace of mind. HBCF is a ‘last resort’ insurance, meaning it only activates when the builder has died, disappeared, or become insolvent. If your builder is still trading but the finish doesn’t meet your standards, Fair Trading NSW acts as the primary body for resolving active disputes. You can’t trigger a claim simply because you’re unhappy with a minor aesthetic detail. The builder must be legally ‘gone’ or have their license suspended for failing to comply with a court order before the fund steps in to provide compensation for completion or repair.

Verification Guide: How to Check Your Builder’s HBCF Status

Protecting your investment is the first step toward creating a true sanctuary. To ensure your project remains a source of joy rather than stress, you must verify your builder’s standing before any soil is turned. The home building compensation fund nsw explained provides a vital safety net, but it only functions if the paperwork is authentic and project-specific. Follow these precise steps to secure your peace of mind.

- Request the Certificate of Insurance before paying any deposit. Under NSW law, builders cannot legally accept a deposit or any payment for residential work valued over A$20,000 without first providing you with this certificate.

- Use the icare HBCF Check portal to verify authenticity. This digital tool allows you to enter the certificate number to confirm it’s genuine. It’s a quick process that prevents the risk of forged documents.

- Cross-reference the builder’s name and licence number. Check the details on the certificate against the NSW Fair Trading public register. The names must match your contract exactly; any discrepancy can complicate future claims.

- Confirm the project address matches your home. A certificate is only valid for the specific site listed. If the address is incorrect or generic, you don’t have coverage for your property.

- File the document safely. This insurance stays with the property for six years for major defects and two years for other defects. It acts as a permanent record that benefits you and any future owners.

Certificate of Eligibility vs. Certificate of Insurance

Think of Eligibility as a builder’s “licence to buy insurance.” It indicates that icare has vetted their financial health and set a limit on how much work they can undertake. However, eligibility isn’t the insurance itself. You must see the project-specific Certificate of Insurance to be protected. A builder having eligibility doesn’t mean your specific project is yet covered, as they must apply for a new policy for every individual contract they sign.

What to Look for on the HBCF Certificate

Examine the finer details to ensure the craftsmanship of your home is fully protected. Verify that the contract price on the certificate aligns with your signed agreement. Check the “description of work” to ensure it accurately reflects your renovation or construction plans. This document serves as a future heirloom, proving to subsequent buyers that the home was built to professional standards. Ensure the dates align with your planned commencement to maintain a seamless transition from planning to construction.

Building with Confidence: Finding Insured Professionals on Patio Market

Elevate your outdoor living by moving beyond the digital mood board and into the reality of a secure, professional build. Transforming a vision into a tangible sanctuary requires more than just an aesthetic eye; it demands a foundation of trust and legal compliance. Patio Market acts as your knowledgeable curator, bridging the gap between high-end design and the practicalities of NSW construction laws. We understand that the transition from a dreamer to a pragmatic buyer is a pivotal moment. It’s the point where you stop imagining the afternoon sun on your skin and start ensuring the hands building your deck are licensed, insured, and reliable.

Choosing a builder who respects the home building compensation fund nsw explained in this guide ensures your investment is shielded from the unexpected. By focusing on verified professionals, you protect the emotional and financial weight you’ve placed on your home. Your outdoor space isn’t just an extension of the floor plan. It’s a destination for well-being, designed for longevity and timeless Australian entertaining.

The Patio Market Advantage: Verified Vendors

Our directory simplifies the search for excellence by connecting you with builders who prioritize both craftsmanship and compliance. We’ve curated a space where searching for the best patio installers leads you to professionals ready to provide HBCF documentation without hesitation. These vendors understand that a seamless transition between indoor and outdoor living requires structural integrity and a commitment to NSW regulatory standards.

- Craftsmanship Focus: Find builders who specialize in weather-resistant materials and UV-stabilized finishes.

- Regulatory Ease: Connect with teams that handle the paperwork for projects exceeding the A$20,000 threshold.

- Quality Assurance: Access a network of experts who view your patio as a future heirloom, built to withstand the harsh Australian climate.

By partnering with professionals who value transparency, you create a sanctuary backed by security. This professional alignment allows you to focus on the sensory details, like the texture of sustainable teak or the flow of a breeze through a new pergola, knowing the legal groundwork is solid.

Next Steps for Your NSW Home Improvement

As you prepare to sign a contract in 2026, use this final checklist to ensure your project begins on the right foot. A successful build is the result of careful selection and clear communication. Browse our extensive listings for outdoor blinds, landscapers, and pool builders to complete your vision; for those also considering climate control upgrades, Peninsula Air Conditioning (PenAir) offers professional solutions tailored to Sydney homes. Before you commit, ensure these three pillars are in place:

- Verify the License: Check the contractor’s current status on the Service NSW public register.

- Secure the Certificate: Confirm you have received the HBCF Certificate of Insurance before paying any deposit over 10 percent.

- Detailed Contracts: Ensure every material specification and timeline is documented in writing to avoid ambiguity.

Your journey toward a more refined lifestyle starts with a single, informed choice. Secure your peace of mind and start building your dream space with the right partners.

Discover NSW’s most trusted patio professionals on Patio Market today.

Build Your Sanctuary with Absolute Certainty

Creating a refined outdoor retreat requires more than an eye for design; it demands a foundation of legal security. Now that you’ve had the home building compensation fund nsw explained, you understand why this insurance is mandatory for any residential project exceeding A$20,000 in value. This essential safety net protects your investment against builder insolvency or license suspension, ensuring your project remains a source of relaxation rather than stress. By verifying your builder’s HBCF status before work begins, you secure the longevity of your high-end craftsmanship.

Patio Market serves as your knowledgeable curator, offering a vetted directory of Australian patio professionals and expert resources on NSW building regulations. We focus on connecting you with experts who understand the nuances of the Australian climate and the importance of durable, weather-resistant materials. It’s time to transform your backyard into a seamless extension of your home with confidence and peace of mind.

Elevate your outdoor living, find a verified NSW patio builder on Patio Market.

Your dream of a perfect, sun-drenched sanctuary is within reach when you partner with professionals who value your peace of mind as much as your aesthetic vision.

Frequently Asked Questions

Is HBCF mandatory for all patio builds in NSW?

HBCF insurance is mandatory for any residential building project in NSW where the contract price exceeds A$20,000 including GST. This threshold ensures your investment in a high-end outdoor sanctuary is protected against unforeseen builder insolvency. If your patio project costs less than A$20,000, the builder isn’t legally required to provide this specific insurance cover.

How much does HBCF insurance cost the homeowner?

The builder pays the premium directly to icare, though this cost is typically passed to you within the total contract price. Premiums fluctuate based on the builder’s risk profile and the project type; however, they generally represent 0.5% to 1.5% of the total construction cost. This small investment secures the longevity of your home improvement, providing peace of mind as you curate your perfect outdoor lifestyle.

Can a builder start work before the HBCF certificate is issued?

No, a builder cannot legally start work or request any deposit payment until they provide you with a valid certificate of insurance. Under the Home Building Act 1989, this document must be in your hands before any physical construction begins on your property. It’s a vital step in ensuring your journey toward a refined outdoor space remains professional and legally compliant.

What happens if my builder goes bust and I don’t have an HBCF certificate?

You’ll lack the primary safety net required to finish your project or fix defects if your builder becomes insolvent without a valid certificate. Without this protection, you become an unsecured creditor in a liquidation process, which rarely results in full recovery of funds. This highlights why the home building compensation fund nsw explained in your contract is a non-negotiable element of any premium renovation.

Does HBCF cover me if I am an owner-builder?

HBCF insurance doesn’t protect you while you’re managing the construction, but it’s required if you sell the property within six years of completing the work. You must provide the buyer with a certificate of insurance to protect them against defects you may have overseen. This ensures the craftsmanship of the home remains a point of value for future owners, maintaining the property’s status as a premium asset.

Does the HBCF insurance stay with the house if I sell it?

Yes, the insurance policy is attached to the property itself and automatically transfers to any new owner within the coverage period. Protection lasts for six years for major structural defects and two years for other less critical issues from the date of completion. This seamless transition of coverage adds significant value to your home, reassuring buyers of the enduring quality of your outdoor sanctuary.

How do I make a claim against the Home Building Compensation Fund?

You initiate a claim through the icare NSW portal once a trigger event occurs, such as the builder’s insolvency, death, or license suspension. You’ll need to provide your original certificate of insurance and evidence of the loss or defect. Having the home building compensation fund nsw explained clearly at the start of your project makes this administrative process much smoother during a stressful time.

What is the maximum amount I can claim from the HBCF in 2026?

The maximum total claim limit currently sits at A$340,000 per dwelling for all losses combined. This figure includes up to 20% of the contract price for non-completion of work. This substantial ceiling ensures that even significant structural failures in a luxury patio or home extension are covered, allowing you to restore your sanctuary without devastating financial loss.